Delta Neutral Trading Explained: The Ultimate Guide to Hedging and Yield Generation

Delta Neutral Trading is one of the most sophisticated yet powerful strategies in the financial and cryptocurrency markets. It allows traders to mitigate directional risk—the risk that the market will move against them—while focusing on generating profits from other factors such as funding rates, volatility (Vega), or time decay (Theta).

In this guide, we will break down exactly what Delta Neutral means, how it works mechanically, and the specific strategies used by institutional investors and quantitative hedge funds to generate "risk-adjusted" returns.

1. What is Delta?

To understand Delta Neutral, you must first understand Delta ($\Delta$).

In finance, Delta is a ratio that compares the change in the price of an asset (usually a derivative) to the corresponding change in the price of the underlying asset.

Spot Assets (e.g., holding 1 BTC): Have a Delta of 1.0. If BTC goes up by $1, your position gains $1.

Short Positions (e.g., Shorting 1 BTC): Have a Delta of -1.0. If BTC goes up by $1, your position loses $1.

Options: Have a Delta between -1.0 and 1.0 depending on whether they are Calls or Puts and how close they are to the strike price.

2. The Core Concept: Net Zero Delta

A Delta Neutral portfolio is constructed so that the sum of all Deltas equals zero.

$$\text{Total Delta} = \sum (\text{Position Delta} \times \text{Size}) \approx 0$$

Why do this?

If your total Delta is zero, your portfolio's total value effectively becomes immune to small price movements of the underlying asset.

If the market pumps +10%, your Long position gains value, but your Short position loses an equal amount. Net Profit/Loss (PnL) from price action = 0.

If you make no money from price movement, how do you profit? The profit comes from Market Inefficiencies and Yield Mechanics, such as:

Funding Rates (in Perpetual Futures).

Basis Spread (Spot vs. Dated Futures).

Option Greeks (Time Decay or Volatility changes).

3. Top Delta Neutral Strategies

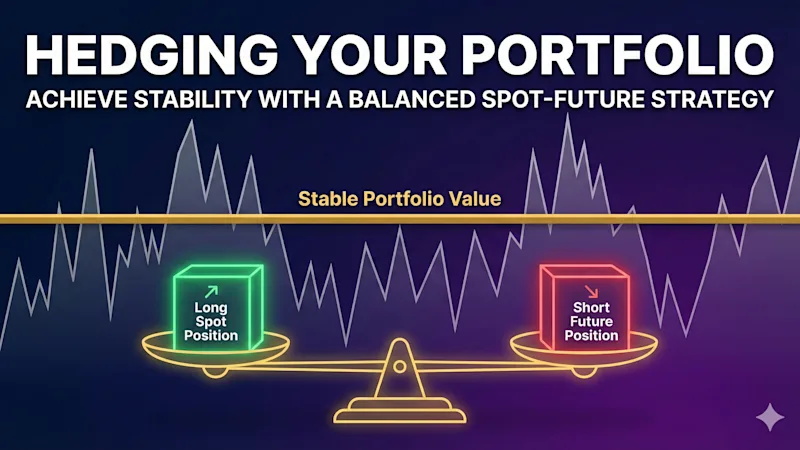

Strategy A: Cash-and-Carry (Funding Rate Arbitrage)

This is the most popular strategy in the Crypto market.

The Setup:

Buy $10,000 worth of Spot Bitcoin (Delta = +1).

Short $10,000 worth of Bitcoin Perpetual Futures (Delta = -1).

Net Delta: 0.

The Profit Source: Funding Rates.

In crypto, perpetual futures prices are tethered to spot prices via a funding rate mechanism. In a bullish market, "Longs pay Shorts."

Since you are holding a Short position, you receive these payments. If the funding rate is 0.01% every 8 hours (approx 10-20% APR), you earn this interest on your position size simply for holding the hedge.

Risk:

Liquidation Risk: If Bitcoin price skyrockets, your Short position could be liquidated if you do not manage your margin collateral properly.

Negative Funding: If the market turns extremely bearish, Shorts may have to pay Longs, eating into profits.

Strategy B: The Calendar Spread (Basis Trading)

Similar to Cash-and-Carry, but using Dated Futures (e.g., BTC Quarterly Futures) instead of Perpetuals.

The Setup:

Buy Spot BTC.

Short a BTC Quarterly Future (e.g., expiring in 3 months) which is trading at a premium (Contango).

The Profit Source:

Futures contracts usually trade at a higher price than Spot. As the expiry date approaches, the Futures price must converge with the Spot price. You capture this difference (the "Basis") as guaranteed profit by the expiration date.

Strategy C: Gamma Scalping (Volatility Trading)

This is a more active strategy often used with Options or Liquidity Provision (LP) in DeFi.

The Concept:

You set up a Delta Neutral position (e.g., a Straddle: Buy Call + Buy Put).

If the price moves aggressively up, your Call gains more value (Delta increases). You now have positive Delta.

To get back to neutral, you sell some of the underlying asset.

If the price drops, your Put gains value. You now have negative Delta.

To get back to neutral, you buy the underlying asset.

The Profit Source:

By constantly "Buying Low" and "Selling High" to rebalance your Delta to zero, you lock in profits from the market's volatility.

Strategy D: Pseudo-Delta Neutral in DeFi (Yield Farming)

Used in Decentralized Finance (DeFi) protocols like Aave or Compound.

The Setup:

Deposit USDC (Stablecoin) as collateral.

Borrow ETH.

Convert that borrowed ETH into a Yield Bearing Asset (like a Liquidity Pool position involving ETH).

The Logic:

Since you owe ETH (a Short debt position) but hold ETH assets (a Long asset position), your exposure to ETH price is neutralized. You profit from the Yield Farming rewards (e.g., UNI, AAVE tokens) and trading fees, minus the borrow interest.

4. Risks and Considerations

While Delta Neutral strategies reduce price risk, they introduce other types of risks:

Execution Risk: When opening a Long and Short simultaneously, a split-second delay (slippage) can mean you don't enter at a perfect 1:1 ratio.

Liquidation Risk: On CEXs, if your short leg moves against you too fast, the exchange may close your position before you can add collateral.

Smart Contract Risk: In DeFi, bugs in the protocol code can lead to total loss of funds, regardless of your perfect hedging strategy.

Rebalancing Costs: Maintaining exactly zero delta requires frequent trading. Trading fees can eat up your arbitrage profits if you rebalance too often.

5. Conclusion

Delta Neutral Trading is not about "predicting the market." It is about mathematical structuring. It transforms trading from a game of gambling on "Up or Down" into a business of extracting yield from market inefficiencies.

For the disciplined trader, it offers a path to consistent, compounding growth, serving as an excellent diversification tool alongside traditional long-term holding.

![[Web3 Native] Create Instant Link Pages with Google! Introducing "cryptolinks.space"](https://images.ctfassets.net/wv6s970ktz13/6U7eMUOuQ0NqxgADqaF3fg/b84d540edc4900ffe5aafbf5c748f334/Gemini_Generated_Image_mb6z0zmb6z0zmb6z.png?fm=webp&w=128&h=128&fit=fill&q=75)